Introduction

Foreign Direct Investments (FDIs) are often a good way for companies to expand their market base and increase their profit margins. However, if a company wants to indulge into foreign investments, certain elements need to be taken into consideration to ensure that the business achieves financial growth. In highlighting these components, the paper investigates Russia’s energy industry to ascertain the prerequisites of investing in a foreign country. Moreover, the paper elaborates on the best type of approach to use in foreign direct investments depending on the host nation’s economic environment. Particularly, this paper will focus on the merging of Centrica, a UK-based oil and gas company, and the Russian energy company Rosneft. The Russian company will be evaluated in terms of its share price, book value, and the corresponding balance sheet to determine its viability to form a merger. Therefore, for a company to indulge in FDI, it needs to assess the macro and micro economic environment of the host nation, the potential of the particular industry, and the best entry method based on the dynamics of the industry.

Best Essay Writing

Services

Need Custon Writen Paper? We'll Write an essay from scratch according to your instructions

Economic Environment Analysis

The economic environment of a host nation comprises both macro and micro environment. The macro environment covers the whole economy as opposed to its specific segments. Elements of the macro environment include the Gross Domestic Product (GDP), Interest Rate, Inflation Rate, and the Balance of Trade (BOT). On the other hand, the micro environment relates to specific segments of the market and includes elements such as customers and supplies, competitors, and the feasible natural environment for investment.

Macro Environment

Gross Domestic Product

Russia is recovering from a great economic recession that occurred due to the drop in oil prices in 2015. Thus, in 2016, the country GDP dropped by 0.2% (Tradingeconomics.com 2017a). However, it subsequently increased by 0.2% and 0.5% within the first and the second quarter of 2017 respectively (Marketrealist.com 2017). Such a positive trend signifies that the country is attracts massive investments to sustain its economy. Additionally, it shows that the companies in the state have a relatively stronger hiring power, which ensures that citizens have enough expendable funds to sustain businesses.

Interest Rate

Russia’s interest rate reached an all-time high of 17% in December 2014 and a record minimum of 5% in June 2010, therefore establishing an average rate of 7.27% within the period (Tradingeconomics.com 2017b). Russia has cut its interest rate from 10% during the first quarter of 2017 to 9.25% by the end of the second quarter (Tradingeconomics.com 2017b). Arguably, a decrease in the interest rate encourages investment, as it reduces the start-up cost of investments.

Inflation

The inflation rate of Russia averaged 4.42% in 2017 (Inflation.eu 2017). The rate has drastically dropped from 0.62% in January to 0.37% by end of April (Statbureau.org 2017). As a result, a decreased inflation rate reduces confusion and creates more certainty in the market, thus encouraging investments.

Balance of Trade(BOT)

Russia’s BOT increased by 21.1%, rising from $6.6 billion to $8 billion within the same month (Focuseconomics.com 2017). Particularly, imports increased from $15.1 to $18.1 billion within the same period (Tradingeconomics.com 2017a). Arguably, this signifies that the domestic demand in Russia is high. Moreover, the decrease in deficit can be attributed to the influx of foreign investors who balance the BOT (Tran & Dinh 2014). Moreover, this shows that the Bank of Russia is spending heavily to increase trade activities in the country.

You can Buy Analysis Essay on this or any other topic at Ninjas-Essays. Don’t waste your time, order now!

Micro Environment

Customers and suppliers

Currently, Russia has an estimated population of 146,419,547 people, which makes it the world’s largest country (Country Meters 2017). Arguably, this wide population offers a very good market for suppliers and customers.

Competitors

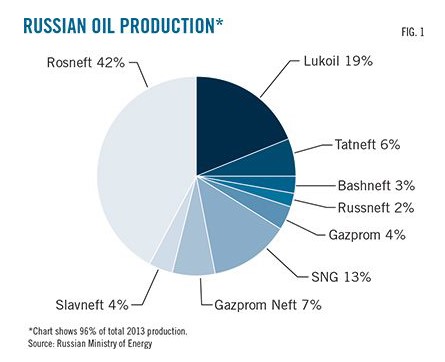

Russia’s energy industry is dominated by a few firms which are highly competitive (See Figure 1). The already existing firms benefit from extensive distribution networks and economies of scale, which allows them to price their products at a cheap price (Eskandari, Meysam & Allahyary 2015). As a result, the entry of new firms is very formidable.

Figure 1. Russian Oil Production (Fjaertoft & Overland 2015).

Feasible natural environment

Russia produces 10% of the world’s total energy. Moreover, its natural gas reserves are the second largest in the world (Clemente 2015). Thus, such abundance in resources encourages massive foreign investments.

Investing in Russia

The best sector to invest in Russia’s energy industry would be the petroleum industry. The reason behind this assertion is that oil ranks among the most important commodity consumed by almost every citizen in the country. Therefore, the guest industry is not only assured of non-limited resources but also unlimited access to suppliers and customers. The best strategy to enter the market would be mergers and acquisitions. To start with, mergers enable companies to diversify and distribute the concentrated risk of their investments (Rashid & Naeem 2017). As a result, Centrica would greatly benefit by merging with the Russian oil company such as Rosneft.

Additionally, mergers and acquisitions help reduce foreign exchange risks that arise from localized recessions in individual countries. Another advantage of using mergers as a strategic entry position is that it enables a weaker company to access debt and equity financing which they were unable to acquire on their own (Peavler 2017). The reason for this is that mergers increase the financial might of the two adjoining companies and make them more competitive (Malik et al. 2014). Furthermore, mergers and acquisitions provide firms with an economic advantage such as the ability to benefit from economies of scale arising from an increased magnitude of operations. Therefore, this mode of entry allows them to price their commodities at a lower value, thus creating a sustainable competitive advantage.

However, although mergers and acquisitions are adequate tools for economic growth, their effectiveness is contingent upon a few factors. To start with, timing is an important factor in forming mergers. Therefore, market dynamics should be observed prior to engaging in a merger. Similarly, mergers fail if the two companies involved have dissimilar corporate culture (Muninarayanappa & Amaladas 2013). Overall, mergers and acquisitions are better as compared to the Greenfield method. The Greenfield method is not preferred for this case since establishing a new corporation in a foreign country is quite costly. In addition, the firm may be faced with various barriers preventing it from accessing the market. Such barriers may arise from high corporate taxes and statutory regulations that bar new firms from entering into the specific industry. Similarly, the Justification and Approval (J&A) model is inappropriate since the legislature of the host country may use this technique to impose harsh conditions, which prevent companies from investing in the country.

Company Valuation

| Centrica | FTSE | |

| Sample Size | 645 | |

| 29/5/2015 to 29/5/2017 | ||

| Maximum Returns | 86.99% | 19.1% |

| Minimum Returns | -38.18% | -1.3% |

| Average Share Price | 200.5 | 3954.995 |

| Average Daily Returns | -7.5% | 0.01% |

| Average Annual Returns | 11% | 10.01% |

| Standard Deviation of Annual Returns | 28.30% | 104.58% |

Figure 2. Centrica’s Valuation (Centrica.com 2017a).

From the above table, it is evident that the maximum and minimum returns of FTSE are not entirely contained by Centrica. Therefore, this signifies that the company’s share price is stable. Moreover, it shows that Centrica’s share price offers more value to shareholders. On the other hand, the close average annual returns of Centrica and FTSE suggests that the company has a high liquidity ratio. Additionally, Centrica has a lower standard deviation on annual returns, which suggests that its investments are less volatile than others in FTSE. Although this analysis can be used in determining FDI, using the book value method is a more appropriate approach.

Figure 3. Centrica’s Share Price (Centrica.com 2017b).

The figure above shows a three-year share price presentation of Centrica’s share prices. From the figure above, it is evident that the company suffered an economic recession in December 2015; however, it is slowly trying to regain its initial position. Arguably, the recession was a result of the drop in oil prices and warm weather.

Book value

The book value for Centrica increased from $1,178 million in 2015 to $2,666 million in 2016 (Centrica.com 2017b). It proves that the value of the company’s assets is depreciating at a slower rate than the accounting requirements which are used to depreciate its value. Therefore, the company’s book value attracts investors because a higher book value proves that the company has a greater liquidity ratio and value in general.

Balance sheet

Centrica had a total debt of $19,158 million in 2015, which decreased to $17,980 million in 2016 (Centrica.com 2017b). Moreover, the company had assets which equalled $19,228 million in 2015 and $21,894 million in 2016 (Centrica.com 2017b). Therefore, the balance increased by $1,178 in 2015 to $2,666 in 2016 (Centrica.com 2017b). Arguably, this signifies an increase in investment and subsequent reduction of liability by the company. Moreover, it proves their credit worthiness, thus attracting investors.

Enterprise value

The enterprise value of a company is calculated by totalling the liabilities presented in the balance sheet and subtracting them from the cash investments, which are also presented in the balance sheet. However, intangible assets are treated as non-cash assets and are not added to the cash investment column. Therefore, the financial model for the company will be as follows.

| Long-term investments | 13,211,000 |

| Property, plant and equipment | 14,395,000 |

| Goodwill | 7,080,000 |

| Intangible assets | 4,368,000 |

| Other assets | 2,107,000 |

| Deferred long-term asset charges | 2,157,000 |

(13,211,000+14,395,000+2,107,000)-(7,080,000+4,368,000+2,157,000)=20,108,100 (This is the enterprise value).

Recommendations

From the analysis above, it is evident that there exists a lucrative business opportunity in Russia’s energy industry. However, tough competition and domination of the industry by a few firms is also a threat to new entrants who wish to trade in the market. Nevertheless, investment in Russia is highly profitable due to the government’s efforts to strengthen the economy after the major recession of 2015, which was caused by oil price fluctuation. However, looking at the vast amount of resources and skilled labour present in Russia, it can be concluded that the benefits of investing in the country by far outweigh the potential risks that are aligned to the investment.

Conclusion

In summary, it is necessary to observe the micro and macro environment of a foreign country before investing in it. In my opinion, the best way to assess such a situation is by continuously observing industrial trends so as to be informed of any significant changes in the market which may affect the investment. Similarly, a company should establish extensive networks within the industry so as to benefit each other mutually and grab more market share. Thus, in order to achieve a high return from investments on FDI, the company must be keen to assess the economic atmosphere of the given country, make inferences, and develop solutions based on the findings they make.